As April approaches, when two Chilean cherry producers meet, the first question they will ask themselves will be: “Do you know anything about the liquidations?” Thus, for a couple of months we are bombarded with information about the results of each exporter. Unfortunately, there are as many fruit liquidation formats as there are exporters on the market, so making comparisons of large averages can lead to serious errors and motivate the producer to make wrong decisions.

Three seasons ago we decided to create a service of Fruit Liquidation Analysis that would allow the producer to be given a report with their approved settlements, including indicators such as: export percentage, category distribution, size distribution, departure dates, prices by variety, prices by size, etc. The idea was that the producer could better understand how their fruit behaves and, at the same time, compare their results year after year, in such a way as to make technical decisions that would allow them to improve certain indicators.

This service has led us to delve deeper into cherry liquidations and better understand which variables most affect the price of this. The approval process has not always been easy, since there are no unique formats; this added to the fact that in recent years not only the variety and the caliber are relevant in prices, the "week" has become a fundamental variable.

Some concepts:

- Export Percentage: This corresponds to the percentage of processed kilos that are actually exported. Here there may be Category 2 fruit or L-sized fruit that often artificially increase the reported export percentage.

- Calibers: The sizes in cherries are separated according to millimeters and are generally tabulated in two ways according to the following table.

- Color: At the time of packing the fruit it is classified into Dark either Light, For labeling purposes, the letter L or D is usually added to the caliber as appropriate. For example, SJL or SJD.

- Category: Fruit that meets the technical specifications for quality and condition to be exported is labeled as Cat1. There are exporters that label Cat2. This fruit can be exported or sometimes sold on the local market. Regarding the L size, in general exporters in recent years do not classify it as Cat1.

- Week: This concept has been fundamental in recent years, since the date on which the fruit is marketed has explained a large part of the result. We have found different ways of detailing this in the liquidations, from the most extreme where there is no detail of the Week, others that detail the Harvest Week or Process Week or Plant Dispatch Week or Sailing Week and if this were not complex enough, there are different calendars of weeks (ISO Calendar or Excel). It is very common to have errors in the reading of liquidations when this concept is not clear and there is still no consensus among exporters on which week should be reported, although it seems that in general the "sailing week" takes the lead.

- Tags: In general, exporters use more than one label for their commercial programs. Many times it may not have to do with the quality of the fruit, but rather with commercial commitments. Therefore, the label is not always clear in showing price differences. Likewise, not all exporters detail their labels at the time of settlement.

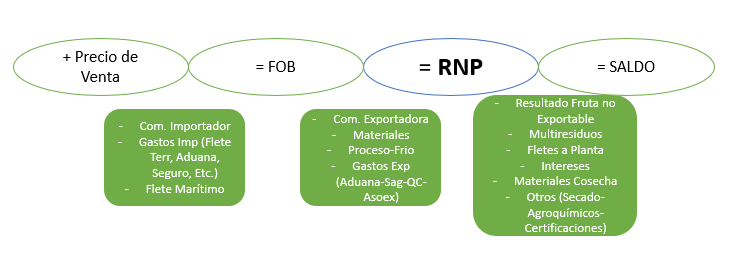

How is the Net Producer Return (NPR) composed?

Fruit sold in destination markets receives a Sale price, from which receiver commissions, destination expenses and maritime freight must be deducted to finally arrive at the FOB price (Free on Board).

From the FOB, the exporter's commission, materials, processing and refrigeration, and export costs must be deducted, to finally arrive at the RNP (Net Producer Return).

In general, exporters report the FOB price, so that they can detail the commission and then show Materials and Services with greater or lesser detail. Although there are also exporters who only report the RNP without giving further details.

Care must be taken when analyzing and comparing costs between FOB and RNP, since it depends on factors such as: type of materials used by each exporter, type of packaging (packaging in small containers is more expensive than bulk packaging), quality of the processing lines, etc. On the other hand, many times an exporter could have higher costs, but with that achieve a higher sale and ultimately deliver a better result, so at the end of the day, the relevant data for producers will always be the RNP.

Non-exportable fruit is normally sold in Chile at very low prices that almost never cover its processing costs. Therefore, in order not to taint the results of exported fruit, an annex detail is provided explaining the costs and income of non-exportable fruit.

Finally, the vast majority details expenses such as Multi-Residue Analysis, Use of Harvest Materials, Interest on advances, Freight, etc. Expenses that are the producer's, but are deducted from the settlement.

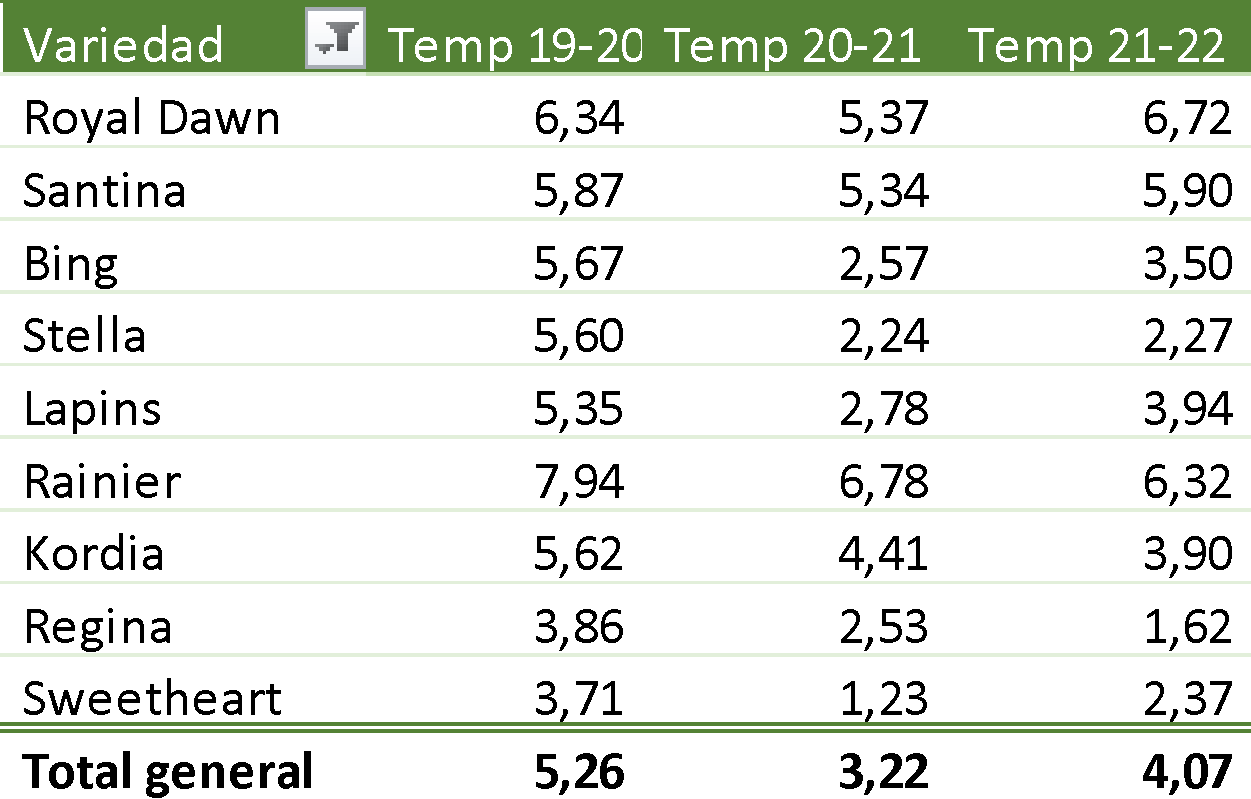

Analysis of the RNP of the last three seasons

Over the last few years we have received and entered settlements into our Database for nearly 9 million kilos annually, providing reports to producers and exporters from different production areas. With this information we have developed a series of tables that show weighted averages using variables such as Variety, Size, Week and Category.

*All Tables are for Cat1 Fruit and do not consider the L Caliber.

Table 1: RNP by Season/Variety

Table 2: RNP by Season/Week

As we can see in the last two tables, early varieties have received a higher premium than mid- and late-season varieties. This has been even more pronounced in the last two seasons, with RNPs of less than USD 2 for fruit from week 1 onwards.

As we know, the caliber is key and as we see in the following tables, larger calibers always pay more. On average, an SJ caliber vs an XL pays more than 2.15 times.

Table 3: RNP by Season/Caliber

As we have seen, weeks and size together explain a good part of the result; the following tables show how the price falls in all sizes and varieties as the season progresses.

Table 4: RNP by Season/Week/Caliber

As we know, size is fundamental, L has already been discarded by many exporters and XL has very low averages, only making it interesting in the first weeks of the season. Last season, XL was already below USD 2 in week 50.

Table 5: RNO by Variety/Week/XL caliber

Table 6: RNO by Variety/Week/SJ Size

Ending the season with a good analysis of the fruit, understanding where the positive and negative points were, in such a way that we can make technical decisions in our orchards to improve export percentages or size curves, as well as comparing year after year how our production evolves, is essential, especially if we want to maintain good profitability; obviously, this analysis must be done not only on cherry trees, but on all the species that a producer has.